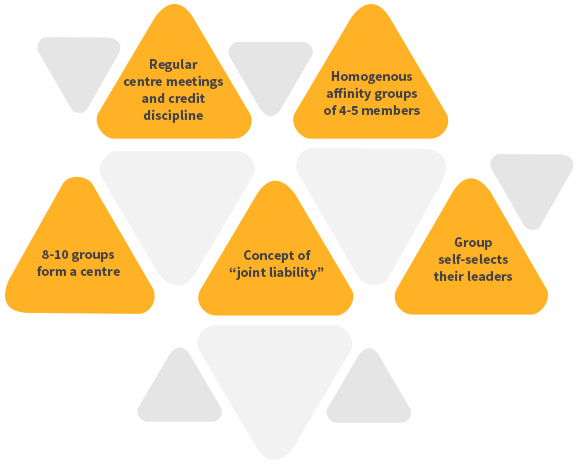

A Micro Finance Institution may lend to individual beneficiaries, or to partner NGOs or to Self Help Groups (SHGs) or allocate funds among these different categories of borrowers.S elf Help Groups:

A Self-help group is a small informal group consisting of not more than 20 members, voluntarily coming together in rural and semi-urban areas. They hold meetings and save small amounts regularly- typically on a weekly basis. The amount is contributed to a common fund and deposited in a bank.

The fund is used to grant collateral-free loans to the members of the SHG.

self help group related to ngo

The groups decide themselves the interest rate and terms for lending from the corpus. Normally these groups lend for very short terms at two to three percent per month working out to 24% to 36% interest per annum. The interest rate depends upon the kind of activity to be pursued by the borrowing member. For instance, the group charges a higher rate if the borrowing is for consumption or non-commercial activities like performing weddings and a lower rate for starting a small business or for the education of children.

The Self Help Group movement has achieved remarkable progress in Andhra Pradesh and Karnataka in its goal of empowerment of women. In Karnataka, womenfolk in rural areas have been organized into self-help groups under the “Sthree Shakti” banner. Many of these SHGs have been credit linked with various banks to provide financial assistance. The State Government has also initiated some noble programs to provide training and orientation to the members on gender issues, communication skills, leadership and skill development in ngo registration process. Some of the women SHGs have also been educated in book-keeping and credit management.

The SHGs are encouraged to take up diverse income generating activities like dairying, manufacturing of ready-made garments, candle-making, petty businesses, production of organic manure, mat-weaving, making of pickle, papads and condiments.

We analyze micro finance institutions(MFIs) as businesses, asking how some MFIs succeed in reducing and covering costs, earning returns, attracting capital, and scaling up. We are interested in MFIs that are financially self-sufficient(covering the cost of daily

operations as well as the cost of capital at a commercial rate or merely operationally self-sufficient (not covering capital costs) or only, say, 90% operationally self-sufficient. All such MFIs strive for efficiency and are in many respects businesslike. Our interest in commercial success does not mean that we believe that it is the reason d’être of microfinance. The ultimate impact on borrowers and communities is what matters for MFI leaders and staffers, as well as for nearly all their investors, by which we mean those who put money in, public or private, through grants, loans, or equity. We focus here on commercial success because viewing MFIs as practical solutions for 80g registration that may result to challenging business problems is a good place to start in understanding why most microfinance operates in the ways it does, what impact it is having, and how it can realistically be expected to enhance its impact.